GP Profile: August Equity Partners

With August Equity Partners nearing 80% of target on its fourth fundraising effort, Denise Ko Genovese talks to managing partner Philip Rattle about strategy and prepping companies for trade buyers

"I spend one third of my time fundraising, one third on new investments and one third on portfolio management," says Philip Rattle, managing partner at August Equity Partners. And with the news that the GP has met 80% of its target for its latest fund, Rattle will soon be able to concentrate on the latter two priorities.

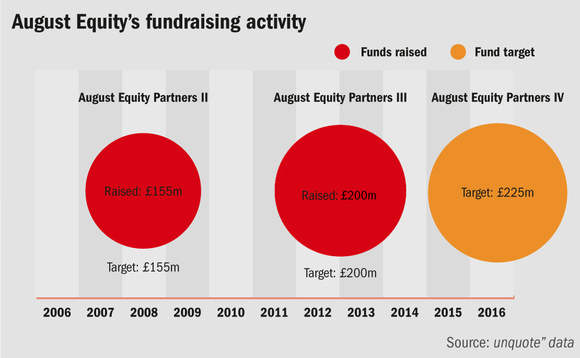

The GP has four funds to date. Fund I closed on £130m in 2003 and is fully realised with a 2.4x return. Fund II raised £155m and is over 90% deployed with a 2.7-2.8x return rate to date. It has a further five investments remaining (three of which are in sale talks). Meanwhile, Fund III raised £200m at final close in 2013 and is 95% committed (the 10th and final investment is imminent). Finally, Fund IV was announced at the beginning of the year and as of July had met 80% of its £225m target, though no official close has been held.

The private equity firm's LP base is fairly diverse and includes a sovereign wealth fund, a UK local authority pension fund, Partners Group and JP Morgan. According to Rattle, the LP base is ever expanding with the latest fundraising efforts bringing five brand new investors to the table.

"We have to be careful to spread allocations out evenly. There were 13 investors in Fund III and we had to make sure none were overweight, as many were keen to commit more," says Rattle.

Trade prep

The recent sale of Funeral Services Partnership (FSP) to Montagu marked the first exit for Fund III. August first acquired FSP as part of a buy-and-build strategy, growing the business to 131 branches from 24 and increasing its profitability almost sixfold from £1.9m to £11m upon exit.

But a sale to another set of private equity hands is not the mainstay of the GP's business. "We typically prepare companies to be sold to trade," says Rattle. "It is our absolute target and comes down to why you want to build the business in the first place."

Rattle adds it is always helpful to have a trade offer even if other sponsors are interested, citing the near sale of supported-living business Lifeways Community Care to a trade buyer in the 2012 sale process. The group's EBITDA grew to £23m in 2012 from £2.1m in 2007, with revenues rising from £23m to £72.5m in that timeframe, and ultimately went to fellow sponsor Omers.

Other investments sold to trade include household products company Rixonway Kitchens, which was sold to Nobia; healthcare provider Enara, sold to Mitie; and software group 4Projects Holdings, sold to Coaxis.

As well as chairing the investment committee, Rattle is responsible for strategic development for the GP. "We have a very clear strategy of building scale in secular markets we know well. We tend to see the US as frequently paving the way for what we can expect over in the UK."

The GP's acquisition last November of UK cloud IT business Wax Digital is a clear example of following US trends. Based in Cheshire, Wax manages £5bn of indirect spend for large and mid-sized organisations and its specialised software helps customers save costs by streamlining their procurement activities.

"The fact that clients have begun to sign up to the software on 3-5 year contracts is definitely ahead of the curve but something that we were already seeing in the US," says Rattle. "Rather than having to buy updated versions of software, you pay a subscription and get access to the whole suite and latest upgrades at any time."

Pet projects

The GP also has an aversion to investing in companies exposed to discretionary spend. While the GP's penchant for animal health businesses – with past deals including Independent Vetcare, Origin, Pet Cremation Services and VetPartners – could seem counter to this, Rattle insists that the sector is not considered discretionary: "It is not comparable to leisure or travel, which are discretionary and less well protected. Perhaps surprisingly, those with pets consider them part of the family and obligatory spend items."

In 2015, the UK spend on pets was £1.5bn, while the total vetcare market is estimated to be worth £3.3bn. Out of the firm's 13 current investments, four are animal health related and on average enjoy 11% like-for-like growth rates. The veterinary model – similar to the funeral sector – lends itself to another common thread of August's investments: small businesses that can be easily scaled.

Origin is a good case in point. The non-domestic veterinary practice has grown from a single site in Sussex when August acquired it in 2000 to now being pan-UK, with the GP helping to consolidate the fragmented market, which is estimated to be worth in excess of £600m.

On average, August invests £10-30m equity per deal with the remaining 40% provided by debt financing, says Rattle. The GP doesn't shy away from direct lenders and is fairly stoic towards their increased presence.

"The [financing] landscape keeps evolving and will continue to do so but financial engineering is not a big driver for us initially at the deal-making stage," says Rattle, implying that August is therefore well insulated. "Before Lehmans it was a heavily institutional and generalist market, but after the crash, funds fell away and others eventually gave up. Those that remain are much more differentiated."

August financed its acquisition of FSP via senior debt from HSBC and a unitranche from direct lender Ares. The GP also used an Ares unitranche for its buyout of VetPartners.

Key People

Philip Rattle, managing partner, joined 3i as a graduate trainee and then moved to JP Morgan Partners. He joined August Equity in 2004 and was appointed to his current role in 2011.

Aatif Haasan, partner, began his career with PwC before moving to Close Brothers Corporate Finance. He joined August Equity in 2005.

David Lonsdale, partner, spent four years in the M&A teams of British Sky Broadcasting and ITV after leaving KPMG's private equity group. He joined August Equity in 2008 and was promoted to his current role in 2013.

Tim Clarke, partner, trained as an accountant with EY and subsequently spent two years with software firm Logica before moving to Kleinwort Benson. He was part of the team that created August in its current form in 2001.

Ian Grant, partner, is a chartered accountant and worked in senior management at Stuart McColl Associates, Babcock Engineering and Fleet Illustrating. In 1989 he joined Kleinwort Bensons's private equity team and joined August in 2001.

More on GPs

IPO offers CVC chance to become multi-asset consolidator

Potential IPO also offers monetisation solution for founders and GP stakes investor Blue Owl

VC Profile: Possible Ventures lines up frontier tech deals halfway through fresh EUR 60m fundraise

Germany-based pre-seed investor is set to hold a first close for its third fund in mid-September

GP Profile: Apheon builds on family roots, mulls exits and reinvestment opportunities

Belgian GP, formerly known as Ergon, to continue to target family- and entrepreneur-owned European businesses

Kudu to step up boutique GP stake deals in Europe

MassMutual-backed investor aims to add more infrastructure and specialised equity GPs to its portfolio

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds