Technology activity holds up despite tough market

Tech deals have remained remarkably robust since the onset of the financial crisis, with fairly consistent deal volumes seen throughout the past few years. However, deal value has fluctuated wildly. Anneken Tappe investigates.

A general downturn in volume and value of private equity deals is neither a new nor a surprising development. Although experts identify technology, pharmaceuticals and healthcare investments as the ‘way to go', investor activity has significantly declined in all three sectors since last year.

While the overall value of healthcare deals remained relatively steady between 2010 and 2011, overall investments in technology and pharmaceuticals slumped by 47% and 76% respectively according to unquote" data. It must be noted that this comparison draws upon numbers of the whole year of 2010 and only three-quarters of 2011. Nonetheless, the indication is obvious: total deal value in the allegedly safe havens of investment is down.

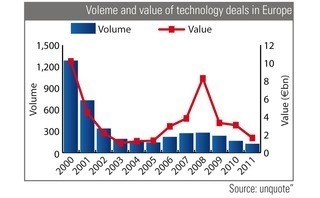

However, data for computer and software investments shows interesting patterns over the past decade. While the value graph slumps upon the burst of the dot-com bubble, it recovers from 2005 onwards in a spiky fashion. Overall value went through the roof in 2008; after the peak, however, it declined as steeply as it had inclined before.

By contrast, the volume curve steadily declined from the turn of the century on and seems to have fluctuated around the benchmark of 200 deals a year ever since then. Admittedly, deal activity rose along with the value surge beginning in 2005, but it has not touched upon the levels seen in the early 2000s.

The spike in the value of tech deals soars from 2005 to 2006, peaking in 2008 and then declining rapidly alongside the rest of the private equity industry. Considering the timing of the financial crisis, which could explain the decline, but not the increase; this begs the question why deal value peaked in 2008. An answer is quickly suggested when separating mega-buyouts. Beginning in 2006, the industry saw a substantial amount of deals valued above €500m. Among those was the €2bn buyout of Skype in 2009 by Silver Lake and Permira's take-private of NDS Group in July 2008, which was valued at €2.3bn. The majority of mega-buyouts were in the software subsector, which includes [online] communication, publishing and distribution tools.

The largest deal of 2011 so far was the acquisition of UK2 Group by Lloyds TSB Development Capital (LDC). The London-based internet business provides website hosting and domain name registration.

If the mid-crisis value peak of tech deals was caused by the relatively small number of mega-buyouts through that time period, the majority of buyouts must have aligned with the low volume levels, which has remained low since 2002. This also means that the plunge in value following the 2008 peak is almost negligible, and most certainly needs to be considered in context. In other words, an internet-giant like Skype won't be sold every single year, which is why the importance attached to average value data should be considered carefully.

Meanwhile, the tech industry appears to be remarkably consistent. Mega-buyouts like the 2009 Skype-deal are obviously distorting value numbers, yet volume has remained remarkably stable following the post-millennium decline. While deal volume in pharmaceuticals and healthcare declined significantly in the past months, the technology sector seems to have the upper hand.

More on UK / Ireland

Inflexion to exit Xtrac in SBO to MiddleGround Capital

Sale of UK-based transmission-systems manufacturer marks Buyout Fund IVтs seventh exit

Federated Hermes raises USD 486m for fifth co-investment fund

Fund surpassed its USD 400m target; its 2018-vintage predecessor raised USD 600m against a USD 350m target

FPE Capital acquires, merges NoBlue and Elevate2

GPтs investment in NetSuite partners marks fifth investment out of third fund

Palatine reaps 6x money on SBO of Anthesis to Carlyle

GP will be reinvesting in UK-headquartered sustainability firm, acquiring a minority stake

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds