Down but not out: UK PE market confident in spite of sterling, macro concerns

Although markets have responded with alarm to the UK governmentтs recent тfiscal eventт, the UK private industry is soldiering on, with opportunities to be had for those who do not see the market as out for the count. Unquote reports on the current market dynamics.

The UK private equity market is no stranger to adapting to the unexpected in recent years, be it Brexit or the lingering consequences of the Covid-19 pandemic. One UK mid-market GP who spoke to Unquote pointed out that the challenges currently faced by the UK are not unique to this market, notwithstanding the recent fiscal event. The euro is also down versus the dollar, with the US currency seen as a safe haven. And supply chain issues, energy prices and inflation woes are by no means only applicable to the UK.

However, it cannot be denied that the "mini budget" has added another layer of complexity to the uncertainty caused by the macroeconomic backdrop. While the Chancellor might have joked in his speech at the Tory Party Conference in Birmingham earlier this week that his plan had caused "a little turbulence", the consequences of this move for the UK private equity industry are too complex to be reversed by a U-turn over the removal of the 45p rate of income tax for higher earners.

Whether current events will make international LPs shy away from the UK as a place to commit their capital remains to be seen. "You could argue it will be a good time to get into a UK fund," said the same mid-market UK sponsor. "It can't get worse, so sponsors can come in low and sell high, since the pound will recover over the next few years."

However, the same source pointed to the cautious nature of LPs, who are already facing tough situations in other markets. "In a world where LPs are already having to ration their capital, it's a good excuse [not to deploy in the UK]," they said.

One private capital adviser told Unquote that they would be "pretty hesitant" to take on a new UK-focused mandate at the moment, although they acknowledged that the market is still in the early days of navigating the situation.

"This situation will stress some portfolios, and if the number of bad apples in a portfolio is overwhelming, this will be a problem," said Tristan Nagler, partner at pan-European carve-out specialist Aurelius. "There is still a lot of capital that wants to find a home in the private equity or private credit environment, and high-quality managers are not available to everyone. But if there is a period of much poorer returns, people might question why they are giving them their money."

Business as usual?

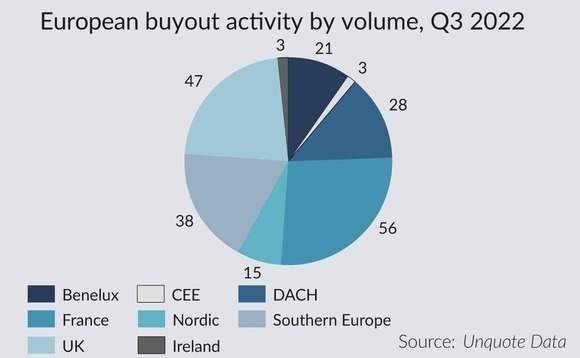

UK dealflow has held up well to date in 2022, in spite of the challenging environment. The aggregate deal value of sponsor-backed buyouts in the UK to date is still 21% up on the total for 2020 and 13% up compare to 2018, according to Unquote Data. Deal volume in the UK in 2022 to date is second only to France, and the country has recorded the highest aggregate value of any region in Europe, accounting for almost a third of aggregate deal value. In Q3 2022, in spite of a drop in activity across all regions of Europe, the UK accounted for 22% of deal volume and 29% of deal value.

Although the picture so far this year has been relatively positive, sellers looking to bring businesses to market now are likely to proceed with caution. One corporate finance adviser told Unquote that those looking to start sale process now will likely test the market before officially launching, meaning that there will be more fireside chats ahead of official process kick-offs.

"In theory, the current situation will drive more dealflow to funds like ours," said Nagler. "Any companies with liquidity issues and heavy leverage will be in trouble. But whether this dealflow will be for transactable businesses that we will have a motivation to support is hard to tell. We are pan-European, so we always question whether we need to do a deal in a certain geography. There is no reason why things can't get worse before they get better."

In spite of this, there are some advantages to treading more carefully, according to David Barbour, partner at FPE Capital. "Sometimes it's worse to be facing a very hot market – abbreviated auctions mean that there is less time to meet management teams and to make reasonable decisions," he said. "In some ways, this is a nicer environment as it means that you can make considered decisions."

Resilient pockets

Total inaction is not an option for private equity, however. While some GPs slowed down their deployment in 2020, they were required to make up for this over the course of 2021 and 2022. Sponsors will need to work out how to navigate the current uncertainty and which businesses to back in this time, looking for resilient pockets of the market.

There are opportunities to be had amidst the doom and gloom. The same mid-market sponsor noted that the bifurcation seen during the Covid-19 pandemic is likely to set up, with the flight to quality meaning that buyers are likely to prioritise businesses with qualities including high pricing power and long-term structural growth. "It would be bad for international investors to shun the UK as some kind of pariah," the same sponsor added, emphasising the significant amount of European dealflow provided by the UK.

The lower mid-market is expected to remain resilient. "Our market has never been reliant on debt and has never got caught up in the headier venture-type valuations," FPE's Barbour told Unquote, highlighting his firm's focus on B2B software and services companies. "History shows that you should invest through difficult times, because that's often when you get the best returns. Generalists might leave the technology sector alone for a while, but we think it will be a good opportunity for investing."

Opportunities are likely to come from owner-run businesses, according to Barbour. "We're seeing strong dealflow around entrepreneurs looking for either growth capital and/or to de-risk – and in some cases complete sales where a business owner wants to cash in or make a retirement sale, given that CGT still comparatively low," he said. "The situation that has developed this year has not stopped people from bringing businesses to the market and we believe strongly that it's still a good time to be investing in low leverage, recurring revenue businesses."

Across the pond

The same corporate finance adviser noted that "savvy US trade buyers and funds" will be taking a close look at the UK market, while the same mid-market sponsor drew parallels to Brexit, noting that this was a time of uncertainty when many US GPs began to infiltrate the UK market.

Recent US entrants to the UK include technology-focused investor Thoma Bravo, which opened a London office in September 2022 headed by ex-Inflexion head of technology Irina Hemmers, as reported. The office opening came amidst speculation about US appetite for listed UK-based technology assets, including cybersecurity software platform Darktrace, although Thoma Bravo subsequently ruled itself out of this process.

"A lot of our exits are to big US software films, who are dollar buyers and probably borrow in dollars, too," Barbour said of the US's role in the UK technology market. "US software houses have raised big funds and have needed to deploy into big platforms, which we've also sold to, and the currency situation increases the attraction of the UK to US buyers. There will be ups and downs in valuations, but the biggest factor will be how desirable a business is, so sector understanding is key."

New market entrants will tread carefully, Aurelius' Nagler noted. "In times of crisis, there are always people who see the opportunity," he said. "But I don't know if GPs will come into the UK who were not already here recently. It's a big strategic move to change geographic focus, and if you don't know the market, you will enter the market, overpay, and overlook why the market is pricing something at a particular level. So the deterioration will have some advantages for those operating in dollars, and the US market is intensely competitive, but new market entrants tend to take a bit of time to build their team and conviction."

What remains clear is UK market participants' conviction on the strength and depth of the UK market. While large-cap buyouts might be on hold in many markets due to the interest rate environments, private equity's long-term view, creativity and drive for returns is likely to see much of the industry through its next big challenge.

More on Investments

Change of mind: Sponsors take to de-listing their own assets

EQT and Cinven seen as bellweather for funds to reassess options for listed assets trading underwater

BHM Group builds on PE strategy, eyes European medtech and renewable energy acquisitions

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Evoco expects portfolio acquisitions, assesses potential exits in 2H23

Switzerland-headquartered GP is currently deploying equity via its EUR 162m Evoco TSE III fund

Turning the tables – an M&A downturn means investment banks are now targets themselves

Some dealmakers with healthy balance sheets and willingness to go countercyclical are pursing acquisitions

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds