VC fundraising sinks further with lowest Q1 in a decade

Amid macroeconomic headwinds, venture capital (VC) fundraising in Europe has reached its lowest first-quarter in aggregate value in a decade, Unquote Data shows.

While VC investment first started to show signs of a slowdown in H1 2022, the collapse of SVB Financial Group, a major startup lender, followed by UBS's rescue of Credit Suisse, have dealt another blow.

Most VCs are therefore investing at a slower pace, with many having large amounts of dry powder left and no immediate need to go to market for new fundraises, KPMG Private Enterprise's Conor Moore told Unquote. Nevertheless, those that were planning to raise new funds in early 2023 have likely put it off in favour of coming back in a less volatile period, said Moore.

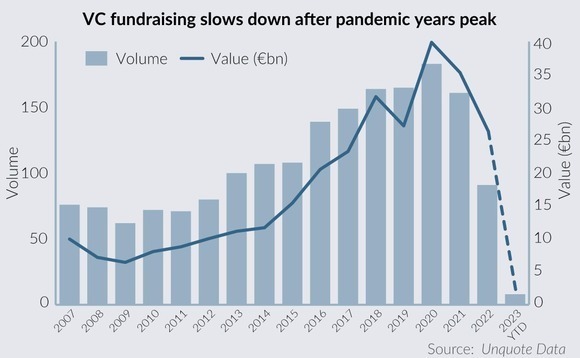

This is borne out by the data, with the aggregate value of venture and growth deals in Q1 2023 down 89% year-on-year, and volume down by 83%, according to Unquote Data.

Globally, there is between five and six quarters' worth of dry powder on the side lines, a record high level, NGP Capital's managing partner Bo Ilsoe told Unquote.

At the same time, the difficult exit environment, with IPO windows remaining largely shut, has suppressed LPs' liquidity and consequently their risk appetite. This has further affected the fundraising efforts of both startups and VCs, especially when it comes to newer, less established entities, added Ilsoe.

In 1Q 2023, eight VC funds completed fundraises, securing a total of just above EUR 2bn in aggregate value, down 50% compared to Q4 2022, according to Unquote Data. Among them is German seed investor High-Tech Gründerfonds (HTGF), which closed its fourth and biggest fund to date on just over EUR 493m in February. This fundraise alone accounts for almost 25% of the quarter's committed capital.

A track record of exits over the course of its two-years fundraising period and the consistent stability of the German government were among the elements in favour of HTGF IV's close, Alex von Frankenberg, managing director of HTGF, told Unquote. The German Federal Ministry for Economic Affairs and Climate Action and KfW Capital, a subsidiary of the German state-owned investment bank, are the fund's anchor investors, as reported.

Slowdown, yet needed

While investment has dropped, alongside startup valuations, all of the market participants who spoke to Unquote said that they view this slowdown as essential.

"It's almost healthy so long as a big financial crisis is not looming," said von Frankenberg, adding that there had to be a slowdown after the peak of 2021 and early 2022.

As the due diligence cycle continues to be extended, founders can leverage VCs' increased caution as a healthy performance incentive to prioritise cost-cutting and operational efficiencies, even generating profitability.

With a positive outlook for IPO windows later in the year as all major US stock indexes move higher lately, and assuming the current economic challenges improve, a recovery is expected between 2H 2023 and 1H 2024, with some volatility expected between quarters, VC practitioners told Unquote.

Typically, it takes somewhere between five to eight quarters for the industry to normalize, as changes are slower in private markets versus the fast corrections seen in public markets, said Ilsoe.

However, the IPO market is limited to an extent by sponsors' and founders' preference to trade sales that generally offer quicker returns on their investment, said von Frankenberg. Moore echoed this view, attributing this tendency to a persistent misalignment between private and public company valuations. However, as prices drop further, M&A activity is likely to pick up, given that those struggling to go for an IPO or receive VC funding might choose different exit routes.

Pockets of activity

Early-stage rounds were previously expected to be the bright spot this quarter and throughout the year, supported by US investors' preference for European startups' lower valuations during Q4 2022, as reported. However, the collapse of SVB might take a toll on US investors' participation in the region going forward, said von Frankenberg. US-based sponsors might be seeking "safer bets" in Silicon Valley as opposed to Europe, said Moore.

Later stage sponsors though, like NGP Capital, which has Nokia as its sole investor, are investing with a longer term horizon. Less interested in short-term market events, NGP Capital bases its investment decisions on a 10-year outlook and is currently bullish on robotics and automation in industrial use cases, as well as generative AI, said Ilsoe.

Moore echoed this, adding that fintech, cybersecurity and "all things defence" are among the top investment areas for VCs in Europe at the moment.

Overall, as funds struggle to secure capital from LPs, now having to compete for capital with more conservative investments such as government securities − which were not profitable when tech startups valuations were higher − trust will be the main aspect determining capital allocations. "There are definitely more choices and more conservatism on the part of the LPs," said Moore.

Obviously, lowering management fees can be attractive, but "it is not going to sway a lot of the investors if they are overallocated or haven't had enough realisations from existing holdings," said Ilsoe. Family offices have more discretion as to how they operate, but most investors will have to choose the managers who will deliver strong returns, he added.

Promising pipeline

Although the amount committed to European VC funds this quarter was only slightly above the EUR 1.2bn total of Q1 2009 − amidst the peak of the great financial crisis − the venture industry has now developed by "leaps and bounds" and is 10 times bigger than it was in the last crisis, said NGP Capital's Ilsoe.

Moreover, the vintages raised during crisis periods tend to perform well with better returns for investors, he added. "The time to invest is between now and 2025 because entrepreneurs are more careful, and given how hard it is to raise capital, startups need to become more capital efficient."

In spite of the slow quarter, the fundraising pipeline shows that a number of VCs are still looking to raise fresh capital for their next vehicles. In the healthcare space, Newton Biocapital, a Belgian-Japanese life sciences VC firm is set to close its second fund by year-end and Spex Ventures' HealthTech Fund has received letters of intent from LPs that it hopes will soon be signed with new allocations becoming available.

Early-stage vehicles are also expected to be raised by VCs, including Spanish firm Nekko Capital, as reported. In addition, UK-based climate impact VC Counteract Partners will close a new decarbonisation-focused fund in December 2023. And in the growth space, Target Global is laying the foundations for its third vehicle.

More on Fundraising

Hayfin exceeds EUR 6bn target for fourth direct lending fund

Firm expects to raise EUR 7bn by year-end as it gears up to meet growing private credit demand in Europe

Unquote Private Equity Podcast: PE perspectives from Berlin

Unquoteтs Min Ho and Rachel Lewis digest the key takeaways from this yearтs SupeReturn

EQT launches semi-liquid strategy for individual investors

Strategy will focus on PE and infrastructure and will be led by ex-Partners Group exec William Vettorato

Wise Equity closes sixth fund on EUR 400m, eyes Italian family-owned B2B targets

Italian GP reached its hard-cap, raising its biggest fund to date four months after launching

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds