Secondary buyout activity stable despite market fears

Despite widespread concern over the number of secondary buyouts being seen in the market, unquoteт research suggests they are no more common today than they were in 2005. John Bakie investigates

Difficult exit market conditions in recent years have created an impression that secondary buyouts were on the rise. Though recent research suggests returns are not significantly lower than those seen in primary deals, there remains concern in the industry and among LPs that they are not an ideal way to acquire new portfolio companies.

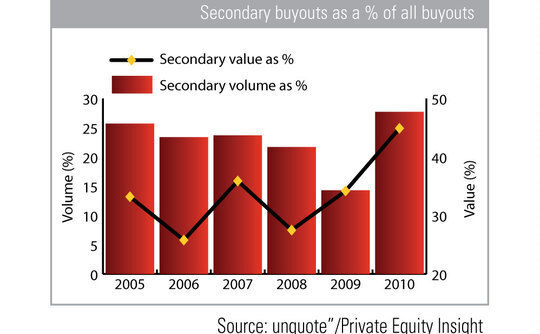

But unquote's own research suggests that secondary buyouts have remained remarkably stable as a percentage of all buyouts. So far in 2010, 27% of all buyouts are secondary transactions. While this represents a substantial increase over 2009, when just 14% of buyouts were secondary transactions, it is broadly consistent with previous years. For example, in 2005 25.7% of buyouts were secondary deals, and in most years since, secondary buyouts make up around a quarter of all buyouts.

The amount of capital invested in secondary buyouts is, on average, higher than that seen in primary deals, but this is to be expected as secondary deals tend to involve more mature companies that have already been built up by another financial buyer. For example, in 2005, while a little over a quarter of deals were secondaries, they represented a third of the market's overall value.

However, while these deals typically account for 25-35% of the whole market by value, their proportional importance has risen substantially in 2010 to 44%. Nevertheless it is likely that this will prove to be the exception rather than the rule, as a number of this year's largest deals have been secondary buyouts. Acquisitions such as that of Picard Surgelés, which was bought for €1.5bn by Lion Capital, or the €1.2bn deal for Ontex will have had a significant impact, distorting this year's figures.

So, while there is still much concern over the role of secondary buyouts, particularly among LPs, the industry does not appear to have been overly reliant on secondary transactions since the financial crisis began. While thish year's increase in the amount of capital entering this market may be of some concern, many of the fears surrounding secondary buyouts could be overblown.

More on UK / Ireland

Inflexion to exit Xtrac in SBO to MiddleGround Capital

Sale of UK-based transmission-systems manufacturer marks Buyout Fund IVтs seventh exit

Federated Hermes raises USD 486m for fifth co-investment fund

Fund surpassed its USD 400m target; its 2018-vintage predecessor raised USD 600m against a USD 350m target

FPE Capital acquires, merges NoBlue and Elevate2

GPтs investment in NetSuite partners marks fifth investment out of third fund

Palatine reaps 6x money on SBO of Anthesis to Carlyle

GP will be reinvesting in UK-headquartered sustainability firm, acquiring a minority stake

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds