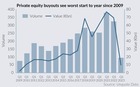

European PE exits back to historic highs in Q1

Emboldened by greater visibility on the pandemic's impact, attractive comparables and PE's strong appetite on the buy-side, GPs divested a near-record number of European assets in Q1 2021, according to Unquote Data.

Unquote recorded 286 exits of European private equity portfolio companies in the first three months of 2021, valued at an estimated aggregate of €75.05bn. While a little shy of Q4 2020's 302 divestments, this makes Q1 2021 the busiest first quarter for exits in volume terms since Q1 2013; it is also the third busiest quarter since 2019, and compares very favourably with the 254 exits recorded per quarter on average across 2016-2018.

The spike in aggregate value was facilitated by a sharp rebound in listings of PE-backed assets at the start of 2021, including several multi-billion flotations for the likes of Auto1, InPost and Dr Martens. In fact, IPOs of PE-backed assets were at their highest in years in the first quarter, with Unquote Data recording 11 such exits.

But buoyed by an equally bullish sentiment on the buy-side for PE, as reported, Q1 also saw a sharp increase in secondary buyout activity, with 91 deals matching the record set in Q2 2018, and the estimated overall value of €28.7bn comfortably exceeding all quarterly totals on record.

Sizeable SBOs in Q1 2021 – also noticeably boosting the record aggregate value of exits in the quarter – included EQT entering exclusive negotiations to acquire France-based medical diagnostics business Cerba HealthCare from Partners Group for €4.5bn, CVC wholly acquiring Danish heavy building materials distributor Stark Group from Lone Star Funds for around €2.5bn, and Charterhouse selling French pharma Cooper Consumer Health to CVC for €2.2bn.

PE divestments were comparatively worse affected by the Covid-19 outbreak last year than incoming investments: the volume of exits by private equity players across Europe fell by 43% year-on-year in Q2 2020 as the coronavirus crisis took hold, as reported at the time. As GPs opted to play it safe and wait for greater visibility on portfolio performance and more post-outbreak comparables to be tempted to launch processes, exit activity also rebounded later than buyout activity, with divestments only starting to accelerate in Q4, whereas incoming investment activity was already healthier by the summer.

While full April figures are not yet available, the fact that the vast majority of Q1's strong exit volume is attributable to March's 127 transactions – making it the second busiest month for exits in the past five years – could indicate that momentum is building up as Europe is starting to contemplate a post-Covid future. That said, it is also likely that a sizeable portion of March's exit activity in the UK (which accounted for a significant portion of the European total) was spurred by a rush to get deals across the line before a mooted hike in capital gains tax rates in the country that month, which ultimately did not come to pass.

More on Data Snapshot

Slice of pie: New entrants gobble up GP stakes in Europe

Armen, Hunter Point Capital, GP House and Axa IM rustle up new minority investments, as Inflexion and Coller sell

Spending bottom dollar: Valuation gaps take Q1 buyout levels back to 2009

Sponsors make just 95 buyouts in Europe in the first quarter - a figure not seen since Sony sold 12m floppy discs in one year

Strategics pull back from PE sales as macro uncertainty bites

Share of trade exits hits lowest point in three years as corporates shore up balance sheets to navigate economic woes

Sidekick spinoffs: Insurtech scale-ups attract PE interest

Investment set to break EUR 1.1bn mark this year as sponsors seek for rising stars

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds