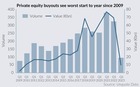

Sponsors kick off 2022 with buyout volume down 13% year-on-year

Buyout volume in the European PE market in January and February 2022 was down 13% on the same period in 2021. With 188 sponsor-led deals, activity fell short of the heights of the 216 seen at the start of 2021, Unquote Data shows.

However, the EUR 46.3bn in aggregate value seen in the first two months of 2022 is a 16% increase year-on-year – and almost equals the record January-February period of 2020. The uptick versus 2021 is due to the increase in average value of deals at the start in 2022, which was almost EUR 250m per deal, versus EUR 185m in the same period in 2021.

A series of large-cap deals were announced at the start of 2022, including PAI and British Columbia Investment Management Corporation (BCIMC)'s USD 8bn sale of Netherlands-based beverage bottler Refresco to KKR in February. In January, Bridgepoint sold UK-headquartered testing, inspection and certification business Element Materials Technology to Temasek Capital for a reported USD 7bn. Many of these saw the winning bidder emerge from a competitive process that had begun in 2021.

While the then-unknown impact of the omicron coronavirus variant took some wind out of the sails of deal-makers at the end of 2021, last year was ultimately a record one for European PE buyout activity, which saw 1,376 buyouts totalling more than EUR 294bn, according to Unquote Data. Overall PE activity last year reached EUR 392bn across 3,765 investments, as reported.

The potential impact of inflation and rising energy costs were on the mind of many sponsors at the start of 2022. However, deal volume was still up 5% compared with the same period in 2020, arguably the last two-month period that saw minimal impact from the coronavirus pandemic. The 188 deals recorded in January and February 2022 also mark a 13% increase on the average seen between 2017 and 2019, meaning that the first two months of the year could be indicative of a return to normal, rather than a true slump in announced deals.

Nevertheless, looking ahead to the rest of 2022, Russia's invasion of Ukraine at the start of March has unleashed a new wave of human suffering and economic uncertainty. Some sale processes are reportedly stalling or being pulled altogether in light of renewed uncertainty. In France, PAI and Baring Private Equity Asia's sale of World Freight Company reportedly ground to a halt due to market volatility.

With many expecting a slowdown in deal announcements as sponsors and advisers take stock of potential targets' exposure to geopolitical and financial risk, it remains to be seen whether deal volume and value in Q1 2022 will represent a return to normal after an extremely busy 2021. Much of the picture for this quarter and the year ahead will depend on the length and progression of the ongoing conflict in Ukraine.

Sponsors' ever-present pressure to deploy is nonetheless likely to mean that any slowdown or deal-doing obstacles are overcome, even if the market faces an initial slowdown. The resilience and strong performance of private equity as an asset class (in particular when compared with public markets) is also likely to remain an underlying driver.

More on Data Snapshot

Slice of pie: New entrants gobble up GP stakes in Europe

Armen, Hunter Point Capital, GP House and Axa IM rustle up new minority investments, as Inflexion and Coller sell

Spending bottom dollar: Valuation gaps take Q1 buyout levels back to 2009

Sponsors make just 95 buyouts in Europe in the first quarter - a figure not seen since Sony sold 12m floppy discs in one year

Strategics pull back from PE sales as macro uncertainty bites

Share of trade exits hits lowest point in three years as corporates shore up balance sheets to navigate economic woes

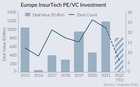

Sidekick spinoffs: Insurtech scale-ups attract PE interest

Investment set to break EUR 1.1bn mark this year as sponsors seek for rising stars

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds