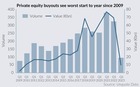

DACH buyouts continue recovery from Q2 2020 low

Figures from Unquote Data show that buyout dealflow in the DACH region has continued to recover from the low point seen in Q2 2020 at the onset of the pandemic.

Aggregate deal value in the DACH region has risen steadily since the three-year low point of €3.6bn across 36 buyouts in Q2 2020.

Q1 2021 saw 54 buyouts totalling almost €14.4bn, an impressive figure considering Q1 2020 saw 42 buyouts totalling €24.5bn, the majority of which was composed of the €17.2bn Thyssenkrupp Elevator buyout. The market is evidently off to a healthy start at the beginning of this year.

In fact, both deal volume and value are now back on par with that seen in Q4 2019, the last pre-pandemic quarter that ended a record year for the DACH region.

Buyouts in Q1 were split almost 50:50 between small-cap deals of less than €50m and deals valued at more than €50m, with smaller deals slightly in the lead. However, this bucks the trend seen in 2020 as a whole, a year in which deals valued at less than €25m alone composed 43% of buyouts by volume, as reported.

In 2020, the DACH region saw six buyouts valued at more than €1bn; three such buyouts have already been recorded in Q1 alone.

In terms of sector, the region saw two large-cap deals in consumer goods and services in Q1; this sector made up more than a third of dealflow by value, with the buyouts of footwear business Birkenstock and eyewear producer Rodenstock accounting for much of this. The basic materials sector is also over-represented by value, although not by deal volume, due to the CHF 4.2bn carve-out of Lonza Specialty ingredients.

According to Unquote sister publication Mergermarket, large-cap processes that are expected to launch in the region in the coming months include BC Partners' sale of pharmaceutical contract business Aenova, as well as Astorg's Switzterland-based industrial software platform Autoform.

In spite of the promising numbers, a rise in coronavirus infection rates in Germany means that the resumption of business as usual is not yet assured, and the pain is not yet over for businesses operating in sectors that suffer significantly under lockdowns. Nevertheless, it is still likely that larger deals will be easier to do in 2021 as market players have adapted to the challenges posed by the pandemic, and vaccination programmes engender a light at the end of the tunnel.

More on Data Snapshot

Slice of pie: New entrants gobble up GP stakes in Europe

Armen, Hunter Point Capital, GP House and Axa IM rustle up new minority investments, as Inflexion and Coller sell

Spending bottom dollar: Valuation gaps take Q1 buyout levels back to 2009

Sponsors make just 95 buyouts in Europe in the first quarter - a figure not seen since Sony sold 12m floppy discs in one year

Strategics pull back from PE sales as macro uncertainty bites

Share of trade exits hits lowest point in three years as corporates shore up balance sheets to navigate economic woes

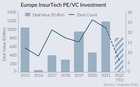

Sidekick spinoffs: Insurtech scale-ups attract PE interest

Investment set to break EUR 1.1bn mark this year as sponsors seek for rising stars

Latest News

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Sponsor acquired the public software group in July 2017 via the same-year vintage Partners Group Global Value 2017

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Czech Republic-headquartered family office is targeting DACH and CEE region deals

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Ex-Rocket Internet leader Bettina Curtze joins Swiss VC firm as partner and CFO

Stonehage Fleming raises USD 130m for largest fund to date, eyes 2024 programme

Estonia-registered VC could bolster LP base with fresh capital from funds-of-funds or pension funds